+5.5% Return Arbitrage in 2 Months - Takeover Play Still On!

Merger arbitrage play yielding +5.5% in 2 months since original post while markets tumble, and counting! Reading time: 7 minutes

Remember that deep dive into Kenmare Resources (LSE: KMR) back on March 10th (Original Article)? Well, a lot has happened since, and despite the market rollercoaster where the S&P is still -8% lower vs its peak, this stock's been quietly delivering. Kenmare’s investors at the time of the article are already making a +5.5% total return in only 2 months, with share price up +2.3% since the article and a 3.2% dividend already deducted from the share price which went ex-div on May 8th. I bought the stock at 392p (~8% return), but I’m not selling - and here’s why. Buckle up for a quickfire update on the takeover process, shareholder returns and financial results.

1. Takeover Tango: Deadline Extension and Insider Buyers

As a quick recap, the takeover bid at 530p per share got a firm "no" initially, but the Board is playing ball, granting additional due diligence access. The "put-up-or-shut-up" clock got a legal extension to May 15th (initially set to April 17th per Irish Takeover Rules). This extension was granted by the Irish Takeover Panel at the request of the Kenmare Board to allow for ongoing discussions and due diligence. Let’s see where Oryx Global and Mr Carvill (Kenmare’s founder and former Managing Director) get to. In the meantime, note that Perpetual Limited (3rd largest shareholder) has been building up its existing stake to ~8.4% of the equity after acquiring additional shares, a strong vote of confidence amidst the uncertainty. L&G also bought additional shares and now owns a 1.3% stake per the regulatory filings.

2. Dividend In The Bag: +3% Free Lunch in 2 months

That final 2024 dividend? It's a done deal: USc17.00 (12.78p) per share, shares went ex-div on May 8th and dividends will hit accounts on May 30th. In addition to the previous interim dividend of USc15.00 (11.27p), this brings the total 2024 dividend to USc32.00 (24.05p) per share, ie. ~6% dividend yield at the current share price which I see as attractive.

Here's the sweet part: despite going ex-div on May 8th (meaning new buyers after that date don't get the dividend), the share price has held steady amid the ongoing takeover, so that's essentially a free 3.2% cash return in 2 months! Together with a share price growth of 2.3%, that’s a 5.5% total return in 2 months .

3. Share Price: Up Despite the Noise

Kenmare is showing remarkable resiliency at a time when the broader market is seeing some serious turbulence following Trump’s tariff announcements. The S&P is still at -8% from the peak while Kenmare’s investors at the time of the article have made a +5.5% total return, with share price up +2.3% since the article on top of the 3.2% dividend already deducted from the share price which went ex-div on May 8th – investors could sell the stock now for a 5.5% gain in 2 months if they wished to as the dividend is already in the bag for shareholders on the register on May 8th (38% in annualized IRR terms, re-investing the proceeds at a similar rate of return). Following Liberation Day and the subsequent market crash, Kenmare's stock saw a temporary dip (down to 353p), but the market quickly recognized that the fundamental value proposition of Kenmare remained entirely intact. Unlike the broader market, which is still grappling with the tariff implications, Kenmare's share price has bounced back and stabilized higher, trading at 411.5p as of last Friday's close. This highlights the market's confidence in Kenmare's intrinsic value and its resilience to wider economic shocks. Keep your eyes peeled for that May 15th takeover deadline which is likely to create share price volatility.

4. 2024 Results & 2025 Guidance

The 2024 results were in line with expectations, with higher volumes and shipments, but lower commodity prices impacting revenues. Management also gave a positive early 2025 picture with production targets intact, strong demand, WCP A upgrade works going as planned and stabilizing ilmenite prices.

2024 results:

Ilmenite production of 1.008,900t increased +2% YoY (986,300t in 2023) and total shipments of 1,088,600t grew +4% (1,045,200t in 2023).

While revenue saw a predictable 10% YoY decrease to $392.1m (from $437.1m) due to softer commodity prices after a bumper 2023 (average ilmenite price has decreased -14% to $360/t vs $418/t in 2023), the key takeaway is pricing stabilization at historically attractive levels – a strong signal for Kenmare's future. EBITDA hit $157.1m, aligning with the ~$153m forecast and confirming our ~3x EV/EBITDA valuation. Even with a material drop in commodity prices and revenues, Kenmare secured a solid ~40% EBITDA margin, showcasing the underlying profitability of its operations.

2025 Guidance:

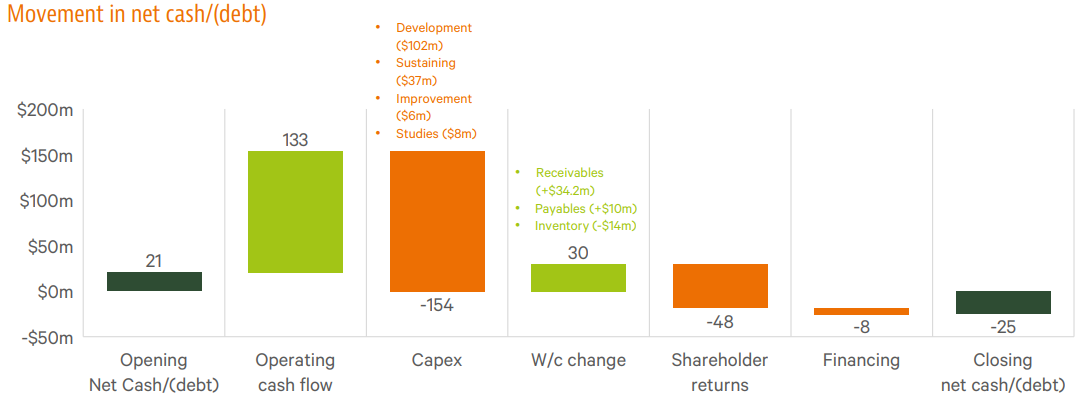

With the crucial WCP A upgrade commissioning in Q3 2025, Kenmare targets robust 2025 ilmenite production of 9,930,000t-1,050,000t. The company invested $154m in CAPEX in 2024, the majority of which was development capex to support the WCP A upgrade ($102m). However, it is so cash generative that it has still maintained a healthy financial position with net debt at $25m, a modest shift from $21m net cash in 2023 (see below a bridge chart highlighting the net debt movements).

Market conditions have been stable in Q1 2025 and Kenmare has a strong order book for its products in 2025.

Ilmenite prices showed signs of stabilization after a weaker 2024.

5. Hold or Sell Now?

Investors who went in at 402p at the time of the original article are up 5.5% in just 2 months post-dividend. I bought shares at 392p, so I am now up almost 8%. Let’s hypothetically assume that I sold it now and deployed the proceeds in a “risk-free” money market fund for the next 10 months, this strategy would yield me a total 12% return in a 12 month period, with close to no risk. However, I have decided to continue holding the stock. Nothing has changed since the original article that in my view impacts the fundamentals of the business, and therefore I’m happy to hold this long-term. Moreover, with the takeover deadline on the 15th, there may by upside through an early exit. What I will say though, is if you’re an investor with a short-term horizon and do not see yourself holding the stock in the long term, beware of the risks of investing now. In 5 days from now, the stock will likely see great volatility – I can see it tanking or increasing massively, depending on what the bidding consortium comes back with by the 15th. For short-term investors focused on quick merger arbitrage deals, one could potentially exit now and realize quick outsized profits and move on to other ideas.

As a recap of the investment thesis, see below the teaser from the (Original Article) as of March 10th:

Merger Arbitrage Opportunity: A recent tender offer at 530 pence per share offers a 32% premium over the current share price (402p). The bidding consortium is led by Kenmare’s founder and ex-Managing Director Michael Carvill, and has been provided with materials to conduct due diligence to improve the offer, as the Board believes 530p/share is not reflective of the company’s intrinsic value

Attractive Valuation in a No-Deal Scenario: At ~3x EV/EBITDA, the business is still attractive even if the deal does not go ahead. Note Kenmare traded consistently above 400p/share for close to 3 years up until late 2023, with recent weakness in the share price mainly due to a large ongoing capex plan due to be largely complete by late 2025/2026

Highly Cash Generative Business: ~19% FCF yield supports growth capex plans and solid shareholder returns (~$280m cumulative since 2019 compared to ~$460m in current market cap)

Resilient Market with Growing Demand and Barriers to New Supply: Favorable long-term demand outlook driven by global GDP growth and urbanization in emerging markets

Long Asset Life: 100+ years of resource life remaining

Disclaimer: The content on this website is for informational and educational purposes only and is not created to meet your personal financial situation. Nothing should be considered as investment advice or as a guarantee of profit. You are advised to consult with your financial advisors to discuss your investment options and whether it would be a suitable investment for your personal needs. The information used in this publication is from sources that are believed to be reliable, but the accuracy cannot be guaranteed. The opinions expressed are those of the author and the author only. These opinions are subject to change without prior notice.

Disclosure: The author currently owns shares of the company here discussed (LSE: KMR) as of May 10, 2025. The security could be sold at any point in time without prior notice.