Supreme – A Growing Consumer Platform at 5.3x EV/EBITDA

Full Investment Thesis: You Don't Want To Miss this!

Following significant interest from our readers after my teaser article posted two months ago (UK Micro-Cap Gem: Doubled EBITDA in 3y), I am excited to provide a comprehensive update on Supreme Plc (AIM: SUP). Since my initial piece, the stock price has increased 17% to 182p in only 2 months, as of Friday’s close (July 4th), and the company has announced a 3.4p dividend (for a total of 5.2p for this fiscal year, i.e. 2.9% dividend yield). While the shares have been trading well and recently touched 205p, I opted to wait for the release of the full-year results last week to provide a comprehensive picture and show you how the company is doing fundamentally rather than celebrating the short-term gains, as I remain a long-term investor in this one.

We've already seen a good leg up in the stock price as investors increasingly realize the market is overly punishing the stock for vaping regulation fears, but the stock remains cheap in my view at 5.3x EV/EBITDA and 8.7x P/E. However, investors should be cautious as there aren’t many near-term catalysts to drive the next leg up in the short term, and shares may be volatile over the next year.

Key Investment Highlights:

Highly Cash Generative Business: Strong and stable free cash flow generation with c. £22m FCF in FY25, representing a 10% FCF yield (excluding M&A capex).

Proven Buy & Build Strategy: Supreme has a strong track record of acquiring and integrating well-established brands into its portfolio (>£25m of acquisitions in FY25 alone) at attractive valuations of c. 5x EBITDA or sometimes even lower

Founder-led Business with >50% Ownership: CEO Sandy Chadha holds a 56% stake in the business, representing the vast majority of his net worth, demonstrating deep commitment and belief in Supreme's long-term prospects. Sandy has an impressive history of identifying new consumer trends and successfully entering new growing segments, having turned a simple distribution business into a powerhouse of consumer brands with a >£200m market cap.

Diversified & Growing Portfolio: Supreme is growing beyond Electricals and Vaping into high-growth areas such as Soft Drinks and Sports Nutrition, reducing reliance on the more mature segments. Supreme more than doubled its revenues in Drinks & Wellness to almost £50m in FY25, and I believe the market does not yet understand the full growth potential for the business both organically and through M&A.

Strong Balance Sheet: The company maintains a very strong balance sheet with net cash of £1.2m in FY25 and an unused £38m credit facility capable of funding capacity expansions and M&A.

Undemanding Valuation: 8.7x P/E and 5.3x EV/EBITDA. The high cash flow supports a decent dividend yield of 2.9% on top of all the capital going to fund capacity expansions and acquisitions.

Rating: Buy

Company Overview

Supreme is a UK-based manufacturer, brand owner, licensee, and distributor of fast-moving consumer goods (FMCG). The company was founded by Sandy Chadha's father in 1975, with the son taking over as CEO in 1988 and leading the company through multiple stages of growth over the few decades and through an IPO in February 2021. Mr. Chadha still holds a 56% stake in the business.

Supreme operates across three main verticals: Electricals (batteries & lighting), Vaping, and Drinks & Wellness. Supreme sells to some of the largest retailers across the UK, including mainstream supermarkets (including Tesco, Sainsbury’s and Morrisons), well-known discount retailers and smaller independent chains. Supreme services approximately 55,000 retail sites, with additional Government & NHS contracts within its Vaping activities. Supreme also sells direct to consumers through its proprietary online sites (e.g., sci-mx.co.uk, sealions.com).

Financials:

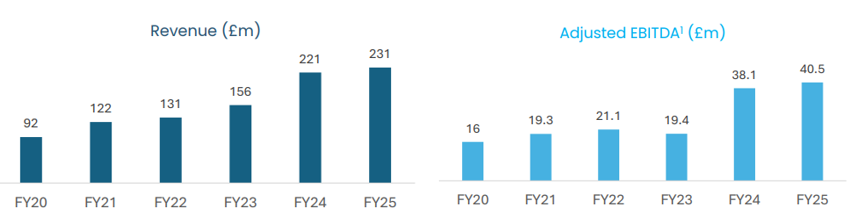

FY25 (ended in March) was a record year for Supreme, with £231.1m in sales (4% annual growth), and £40.5m in adj. EBITDA (up 6% YoY) despite the disruption caused by the new UK regulation impacting the Vaping segment. Supreme’s gross margin expanded by +320bps to 31.9%, and EPS increased by 6.2% YoY to 21.0p (FY24A 19.8p). The Group maintained a policy of distributing c. 25% of net profit in dividends, proposing a total dividend of 5.2p in FY25 (up from 4.7p in FY24).

Supreme operates through 3 core verticals:

1. Drinks & Wellness (~20% of Gross Profit) – Since 2018: This is the newest and strategically most important vertical, expected to drive the bulk of the growth. It was formed by combining the former Sports Nutrition & Wellness (SN&W) activities with the recent strategic acquisitions in Soft Drinks and Hot Beverages made in 2024. Total sales in this new category more than doubled to £48.8 million in FY25, driven by the 2 large acquisitions in the Drinks space, with underlying growth also in the former Sports Nutrition and Wellness activities. This segment is anticipated to be a primary driver of future growth for Supreme, lessening the company's dependency on the more mature Electricals and Vaping segments over time. I’ve added some background on the category below, if you know this already you can skip to the next vertical.

Supreme entered the Sports Nutrition & Wellness category in February 2018, later bolstering its position with bolt-on acquisitions such as Battle Bites protein bars (October 2020), and the Sci-MX and Pro2Go brands (July 2021). This category, now a component of the broader Drinks & Wellness segment, had recently faced some challenges due to cost inflation in raw materials like dairy. However, FY25 brought a welcome easing of these cost pressures, which supported a 5% growth in sales and a rebound in gross margins, underpinned by strong growth from the Sci-MX brand. The commissioning of new production facilities are expected to secure new contract wins and double-digit sales growth is expected in FY26F, with further progress anticipated in FY27F, per brokers’ estimates.

The Soft Drinks vertical was established in June 2024 through the £15m acquisition of Clearly Drinks, which is a well-established UK brand of soft drinks and spring water with 140 years of history (brands include Perfectly Clear, Northumbria Spring, and Revolution Waves. Clearly drinks had generated c. £3m in EBITDA in FY23, meaning Surpeme paid c. 5x EV/EBITDA which is undemanding and justified by the growth – this was fully funded with free cash available). Supreme then further expanded into Hot Beverages with the acquisition of the well-known British grocery brand Typhoo Tea for £10m in December 2024, having moved very quickly in a difficult insolvency situation where Management believes the business was acquired on the cheap (the inventory stock and trade debtors alone had a book value of £7.5m which was washed in the transaction). Typhoo Tea generated sales of c. £20m last year and Supreme believes it can generate c. 30% gross margins under its ownership (~£6m gross profit, which could mean c. £4-5m in EBITDA, meaning Supreme effectively paid c.2x EV/EBITDA for this business if it manages to turn it around).

Key Segment Brands:

Segment Financials:

2. Electricals (~15% of Gross Profit) – Since 1989: Supreme boasts a c. 35-year history in battery distribution, and this category served as the base from which the Group's verticals have been built. It has built long-standing, well-established relationships and distribution agreements with leading brands in the category, including Panasonic batteries (approximately 31 years), Duracell (approximately 30 years), and Energizer (approximately 26 years). In FY25, Supreme supplied over 350 million batteries across the UK, maintaining a 35% market share. This segment is a stable, highly cash generative and relatively low maintenance, benefiting from long-established customer relationships. This segment also includes Lighting, where Supreme operates as a licensed distributor since 2009. It is highly complementary to the existing Batteries business due to established retail relationships and distributes leading brands such as Black+Decker, Energizer, Eveready, and JCB. I don’t expect growth to come from this legacy category (sales were down 6% YoY and this trend is not likely to be reversed materially) given the secular pressures on both volumes and pricing. However, investors should see this segment purely as a cash cow that is funding growth in other areas of the business (funded Supreme’s very successful entry into Vaping over 10 years ago, and is now funding the growth into Drinks & Wellness). In fact, this is how Supreme has managed to invest >£25m in the 2 strategic acquisitions in the Drinks & Wellness segment and continued to pay dividends without accumulating a pile of debt (net cash position of £1.2m).

Key Segment Brands:

Segment Financials:

3. Vaping (~64% of Gross Profit) – Since 2013: Supreme is estimated to produce c. 30% of the total e-liquid volumes in the UK. The company entered the Vaping category in 2013 through the KiK and 88Vape brands and added manufacturing capacity at its existing facility in Trafford Park, which produces 320,000 bottles of vaping e-liquid every day for its own brands and third parties. The company's position in the category has been strengthened through acquisitions of vaping brands like Liberty Flights (June 2022), Cuts Ice (August 2022), and Superdragon (March 2023). The scale and network that Supreme has built with key UK customers (including Tesco, Sainsbury’s and Morrisons) also allowed the company to sign an exclusive master distribution agreement for ElfBar and Lost Mary disposable vapes in the UK in FY24A, significantly transforming the scale of its vaping business. Note these exclusive agreements have a much lower margin as Supreme acts solely as a distributor.

Regulatory tailwinds are the name of the game in UK vaping and may cause short term pain. However, as I explain in my previous article (UK Micro-Cap Gem: Doubled EBITDA in 3y), I believe 1) that those risks are overblown as new products have already come out recently that comply with the disposable vapes regulation and which look identical to the consumer, and 2) that Supreme is in a great position to navigate these regulatory changes, and may even benefit if it manages to consolidate struggling brands in this fragmented market. Vaping revenues declined 8% YoY to £129m in FY25 from the FY24 peak amidst these regulatory tailwinds, and may continue to see pressure in the following quarters.

Key Segment Brands:

Segment Financials:

Valuation

At the current share price of 182p, Supreme trades at 5.3x EV/EBITDA and 8.7x P/E, with a market capitalization of c. £213m (and EV of c. £212m given the ~£1m net cash position). This looks cheap compared to peers, in any comp set one may choose to use:

Major distributors like Travis Perkins, Diploma, Bunzl, etc. trade average multiples of c. 11x EV/EBITDA and 15x P/E

Soft drink companies including PepsiCo, Coca-Cola, Fevertree, etc. trade at average multiples of c. 13x EV/EBITDA and 15x P/E

Even within the tobacco sector, companies like BATS, Philip Morris, Altria, and Imperial Brands, trade at c. 9x EV/EBITDA and 12x P/E

Consumer staples giants such as Unilever, P&G, Nestle, Walmart, PepsiCo, and Reckitt command average multiples of c. 12x EV/EBITDA and 21x P/E

Supreme stock is trading at a notable discount compared to peers. And while I understand a smaller business like Supreme should not trade at the same multiple as a Travis Perkins or a Philip Morris, the current valuation is so low in my view that there is plenty of room for upside. While the near-term future for Supreme may involve some patchy and tough navigation, particularly concerning the new vaping regulation, the current valuation is attractive for a business of this quality in my view. The Drinks & Wellness segment is well positioned to drive significant growth, and while Electricals and Vaping categories may face tailwinds as discussed above, they serve as reliable cash cows that can continue to fund the next areas of growth, both organically and inorganically. Cash flow can be strategically reinvested to fund future acquisitions in emerging, higher-growth areas like Drinks & Wellness, or other new segments management identifies, as they have successfully done many times in the past.

A Quick Appendix Note: UK Vaping Regulation

The UK vaping market has recently undergone significant regulatory changes, with more on the horizon. A ban on disposable vapes came into effect in June 2025 in the UK and Ireland. This led Supreme to consciously 'de-emphasize' its disposable 88Vape SKUs and reduce stock holdings ahead of this date, resulting in a decline in sales, but non-disposable vaping saw continued growth of approximately 8%. Looking ahead, a major new regulation will impact the category from October 2026, when excise duty will be levied on all vaping products at £2.20 per 10ml, impact of which is still to be understood.

Despite these regulations, the demand for nicotine products tends to be very sticky, suggesting vaping is unlikely to disappear. For an average smoker of 10 cigarettes per day, switching to refillable vapes can result in over £2,000 in annual savings, making them a significantly more affordable alternative to traditional cigarettes. Even with the ban on disposable vapes, management expects more than 50% of that demand to transition to rechargeable pods, and Supreme is well-positioned to gain market share in this evolving landscape due to its existing market share in e-liquids for reusable vapes. While initial impacts on demand are expected to be temporary, the introduction of this excise duty may also prove to be an opportunity of considerable scale for Supreme, potentially driving a consolidation in what is a highly fragmented market as smaller manufacturers face increased cash and manufacturing burdens.

Conclusion

Despite a likely modest decline in organic sales in the coming year, I see continued growth opportunities through M&A and organic growth in Drinks & Wellness, which for a c.5x EV/EBITDA valuation seems attractive over the long-term - even if shares may suffer over the next year. Despite temporary impacts on volumes across the market, profitability is expected to materially hold up and provide key support to future growth. Outside of vaping, Supreme's broad, deep, and long-standing relationships are expected to drive medium to long-term growth across its categories, supported by ongoing bolt-on/corporate activity. As I mentioned in my previous article, I have been an investor in Supreme for a while now and I continue to hold a meaningful position in the stock, which I will continue to monitor and may buy more if shares see a downward correction over the course of this year.

Disclaimer: The content presented on this website is strictly for informational and educational use. It should not be considered as financial or investment advice, nor does it guarantee any profit. While we strive for accuracy, errors may be present; please conduct your own due diligence. Opinions expressed are the author's own and may change without notice.

Disclosure: At the time of this article's publication, the author holds shares in Supreme Plc. This position may be altered or liquidated at any time without prior notification.